Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeEnergy Storage Arbitrage in Real-Time Markets via Reinforcement Learning

Feb 23, 2018

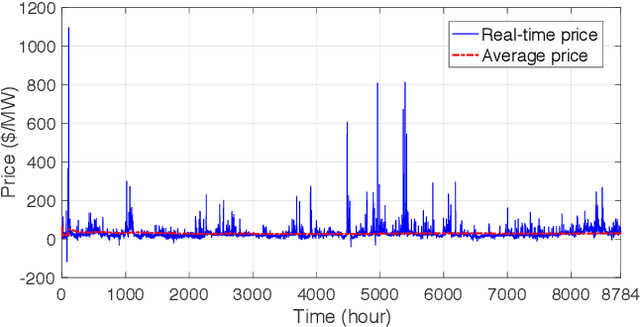

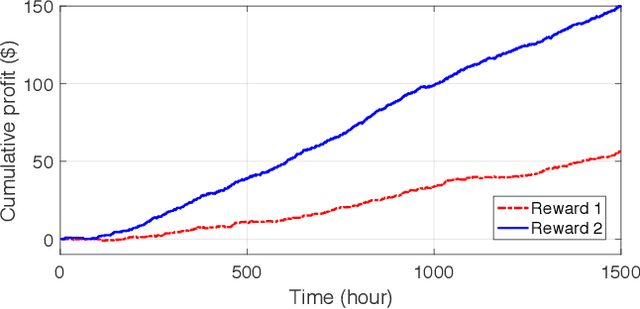

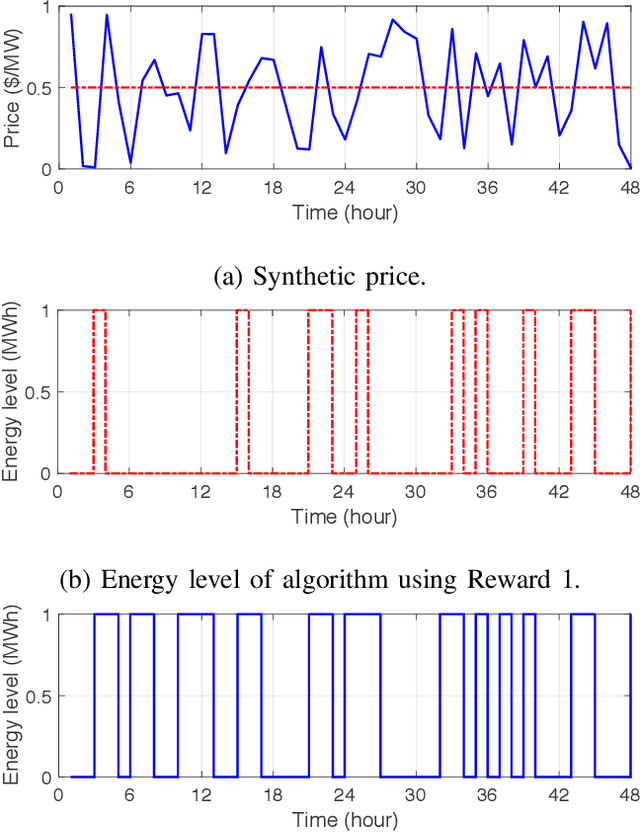

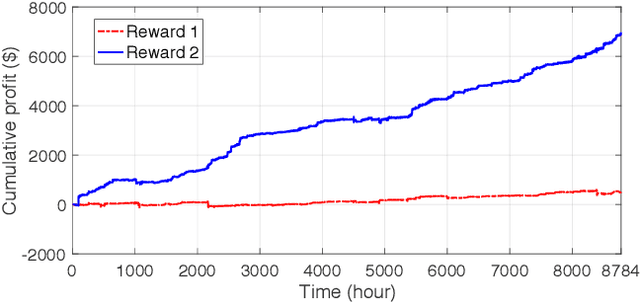

In this paper, we derive a temporal arbitrage policy for storage via reinforcement learning. Real-time price arbitrage is an important source of revenue for storage units, but designing good strategies have proven to be difficult because of the highly uncertain nature of the prices. Instead of current model predictive or dynamic programming approaches, we use reinforcement learning to design an optimal arbitrage policy. This policy is learned through repeated charge and discharge actions performed by the storage unit through updating a value matrix. We design a reward function that does not only reflect the instant profit of charge/discharge decisions but also incorporate the history information. Simulation results demonstrate that our designed reward function leads to significant performance improvement compared with existing algorithms.