Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeModeling default rate in P2P lending via LSTM

Feb 13, 2019

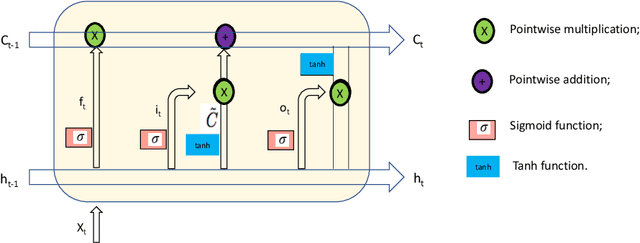

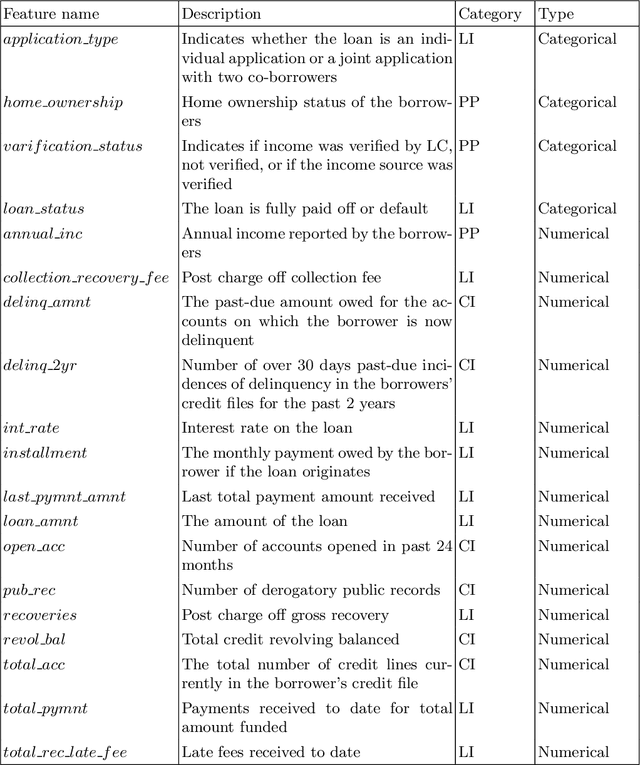

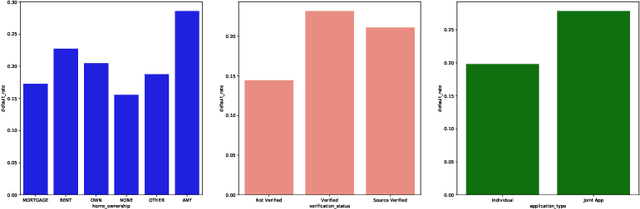

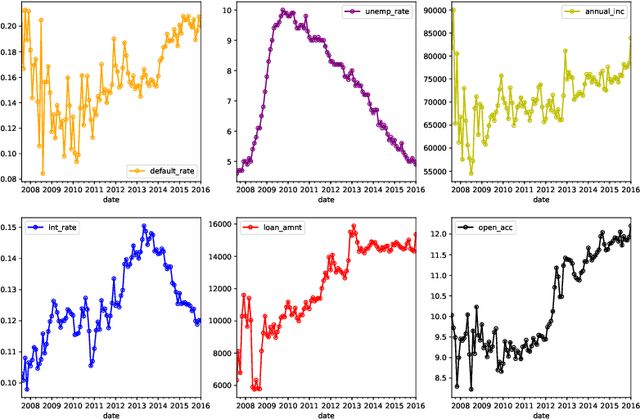

With the fast development of peer to peer (P2P) lending, financial institutions have a substantial challenge from benefit loss due to the delinquent behaviors of the money borrowers. Therefore, having a comprehensive understanding of the changing trend of the default rate in the P2P domain is crucial. In this paper, we comprehensively study the changing trend of the default rate of P2P USA market at the aggregative level from August 2007 to January 2016. From the data visualization perspective, we found that three features, including delinq_2yrs, recoveries, and collection_recovery_fee, could potentially increase the default rate. The long short-term memory (LSTM) approach shows its great potential in modeling the P2P transaction data. Furthermore, incorporating the macroeconomic feature unemp_rate can improve the LSTM performance by decreasing RMSE on both training and testing datasets. Our study can broaden the applications of LSTM approach in the P2P market.