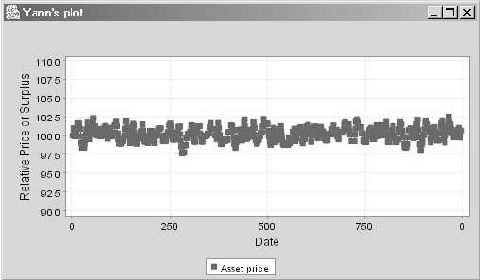

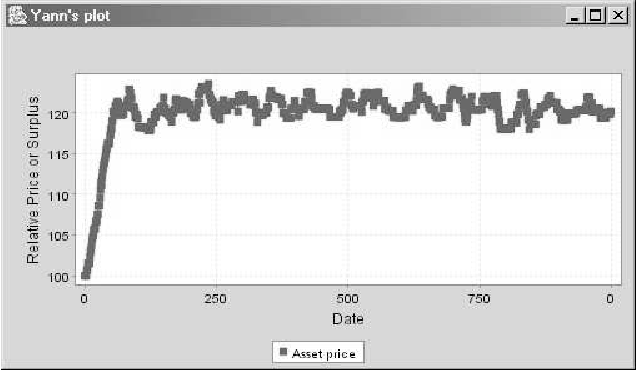

Pertaining to Agent-based Computational Economics (ACE), this work presents two models for the rise and downfall of speculative bubbles through an exchange price fixing based on double auction mechanisms. The first model is based on a finite time horizon context, where the expected dividends decrease along time. The second model follows the {\em greater fool} hypothesis; the agent behaviour depends on the comparison of the estimated risk with the greater fool's. Simulations shed some light on the influent parameters and the necessary conditions for the apparition of speculative bubbles in an asset market within the considered framework.

🔥 Discover incredible developments in machine intelligence

🤖 Quickly get code for any ML model

🔑 Get help from authors, engineers & researchers

Add to Chrome

Add to Chrome

Add to Firefox

Add to Firefox