Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeLi-Xin Wang

A Fast Training Algorithm for Deep Convolutional Fuzzy Systems with Application to Stock Index Prediction

Dec 07, 2018

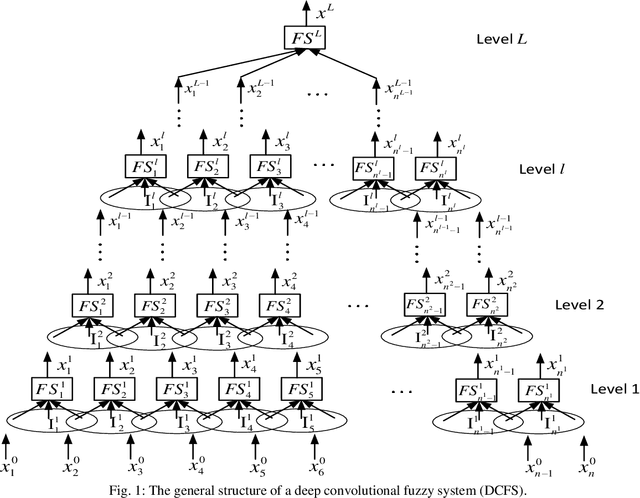

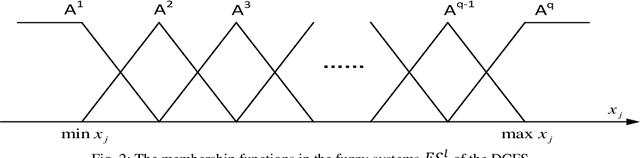

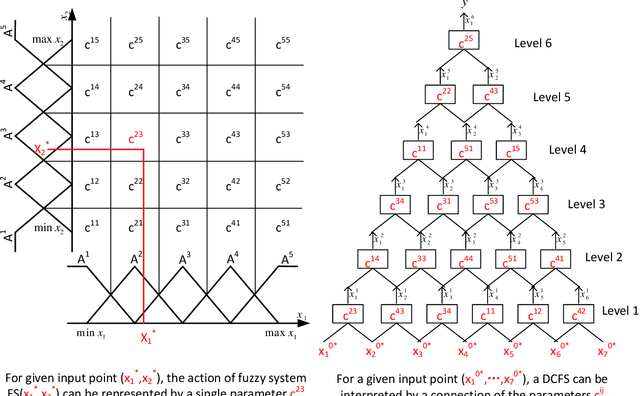

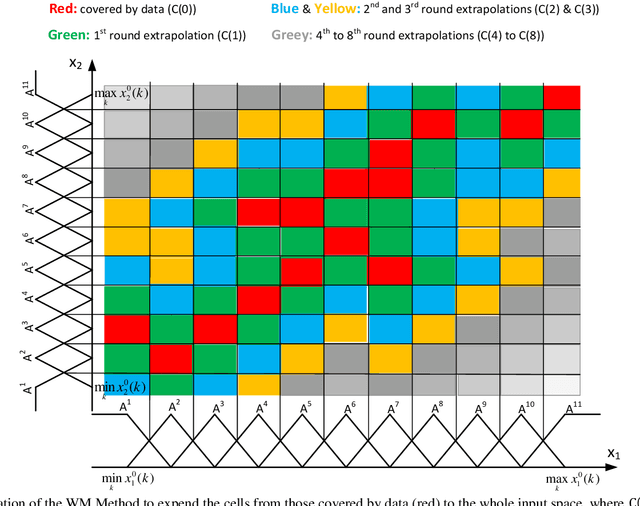

A deep convolutional fuzzy system (DCFS) on a high-dimensional input space is a multi-layer connection of many low-dimensional fuzzy systems, where the input variables to the low-dimensional fuzzy systems are selected through a moving window (a convolution operator) across the input spaces of the layers. To design the DCFS based on input-output data pairs, we propose a bottom-up layer-by-layer scheme. Specifically, by viewing each of the first-layer fuzzy systems as a weak estimator of the output based only on a very small portion of the input variables, we can design these fuzzy systems using the WM Method. After the first-layer fuzzy systems are designed, we pass the data through the first layer and replace the inputs in the original data set by the corresponding outputs of the first layer to form a new data set, then we design the second-layer fuzzy systems based on this new data set in the same way as designing the first-layer fuzzy systems. Repeating this process we design the whole DCFS. Since the WM Method requires only one-pass of the data, this training algorithm for the DCFS is very fast. We apply the DCFS model with the training algorithm to predict a synthetic chaotic plus random time-series and the real Hang Seng Index of the Hong Kong stock market.

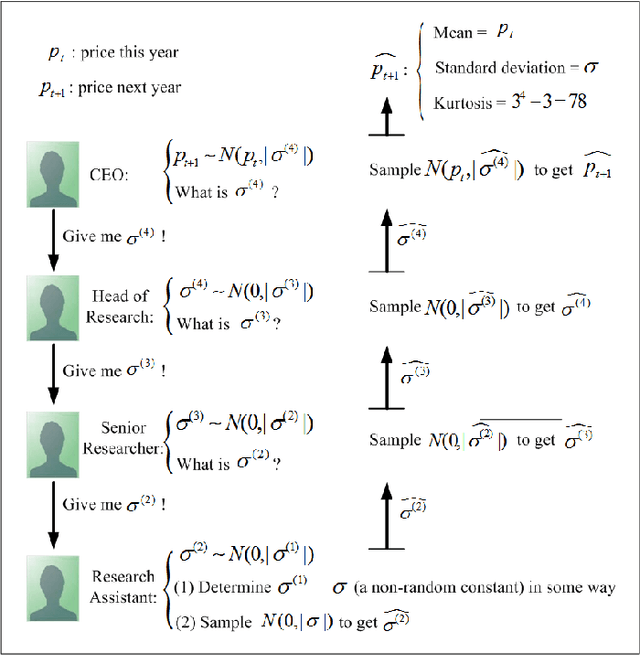

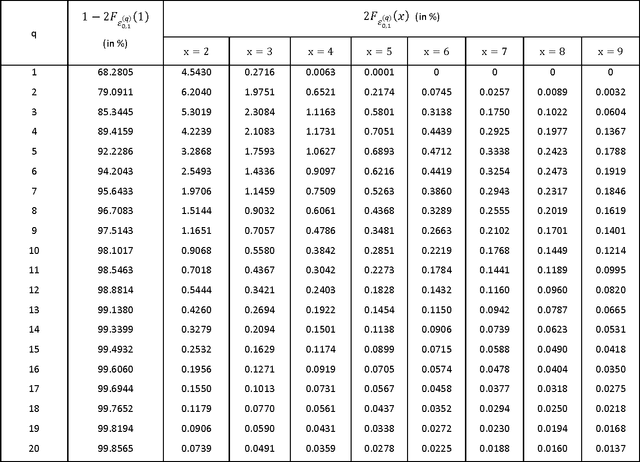

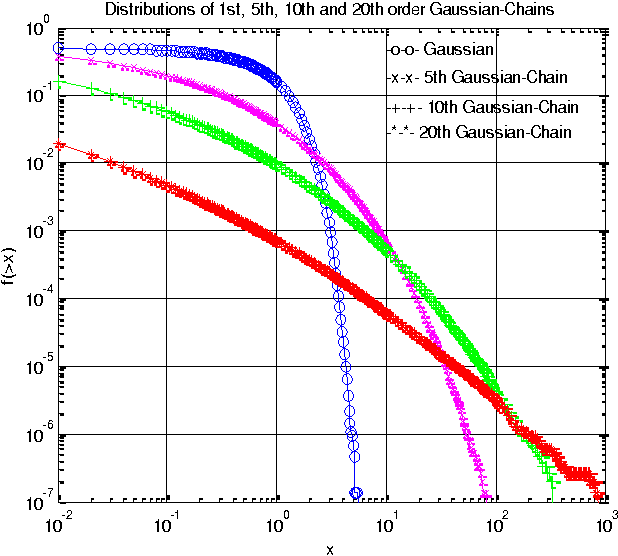

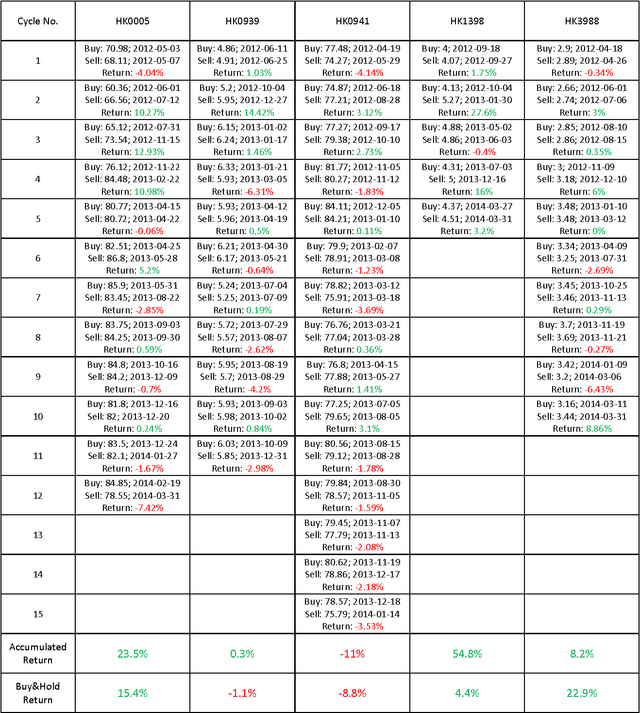

Gaussian-Chain Filters for Heavy-Tailed Noise with Application to Detecting Big Buyers and Big Sellers in Stock Market

May 09, 2014

We propose a new heavy-tailed distribution --- Gaussian-Chain (GC) distribution, which is inspirited by the hierarchical structures prevailing in social organizations. We determine the mean, variance and kurtosis of the Gaussian-Chain distribution to show its heavy-tailed property, and compute the tail distribution table to give specific numbers showing how heavy is the heavy-tails. To filter out the heavy-tailed noise, we construct two filters --- 2nd and 3rd-order GC filters --- based on the maximum likelihood principle. Simulation results show that the GC filters perform much better than the benchmark least-squares algorithm when the noise is heavy-tail distributed. Using the GC filters, we propose a trading strategy, named Ride-the-Mood, to follow the mood of the market by detecting the actions of the big buyers and the big sellers in the market based on the noisy, heavy-tailed price data. Application of the Ride-the-Mood strategy to five blue-chip Hong Kong stocks over the recent two-year period from April 2, 2012 to March 31, 2014 shows that their returns are higher than the returns of the benchmark Buy-and-Hold strategy and the Hang Seng Index Fund.