Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRen-Jie Han

Long Short-Term Memory Networks for CSI300 Volatility Prediction with Baidu Search Volume

May 29, 2018

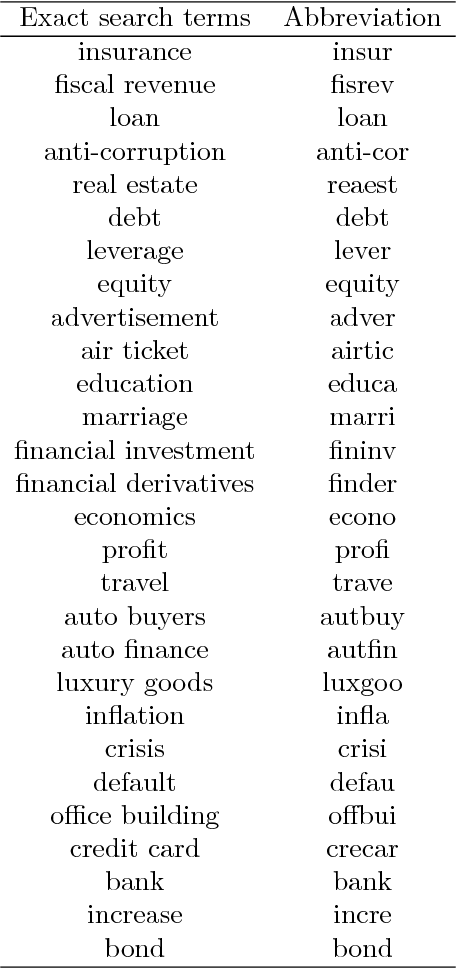

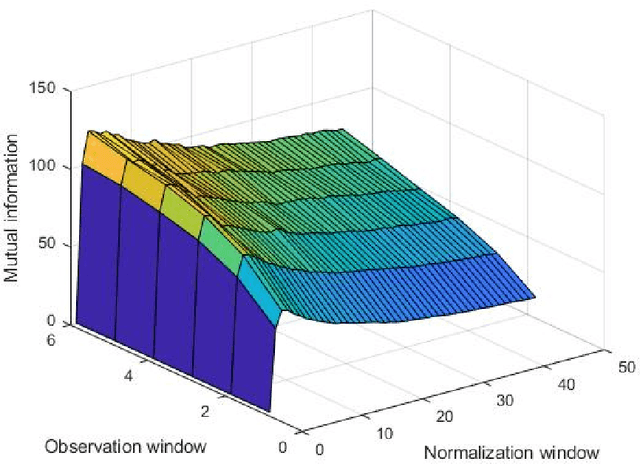

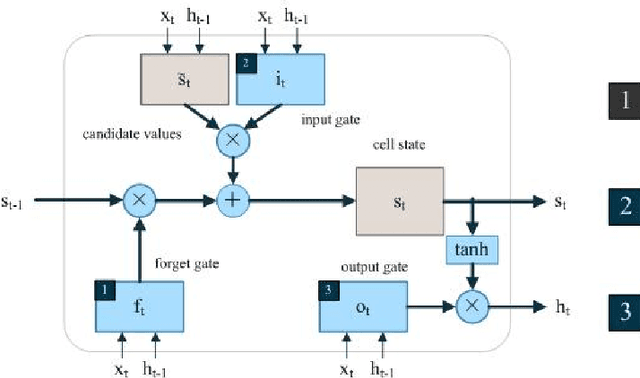

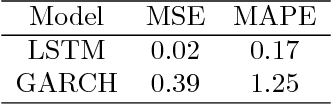

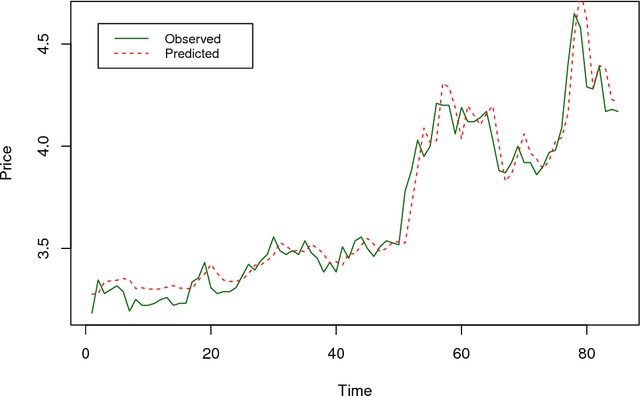

Intense volatility in financial markets affect humans worldwide. Therefore, relatively accurate prediction of volatility is critical. We suggest that massive data sources resulting from human interaction with the Internet may offer a new perspective on the behavior of market participants in periods of large market movements. First we select 28 key words, which are related to finance as indicators of the public mood and macroeconomic factors. Then those 28 words of the daily search volume based on Baidu index are collected manually, from June 1, 2006 to October 29, 2017. We apply a Long Short-Term Memory neural network to forecast CSI300 volatility using those search volume data. Compared to the benchmark GARCH model, our forecast is more accurate, which demonstrates the effectiveness of the LSTM neural network in volatility forecasting.

Neural networks for stock price prediction

May 29, 2018

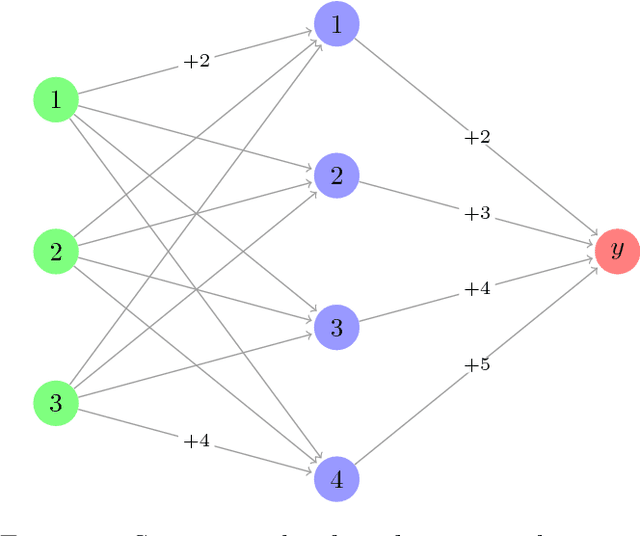

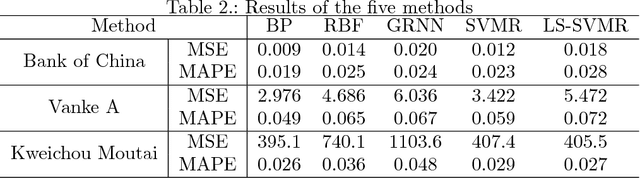

Due to the extremely volatile nature of financial markets, it is commonly accepted that stock price prediction is a task full of challenge. However in order to make profits or understand the essence of equity market, numerous market participants or researchers try to forecast stock price using various statistical, econometric or even neural network models. In this work, we survey and compare the predictive power of five neural network models, namely, back propagation (BP) neural network, radial basis function (RBF) neural network, general regression neural network (GRNN), support vector machine regression (SVMR), least squares support vector machine regresssion (LS-SVMR). We apply the five models to make price prediction of three individual stocks, namely, Bank of China, Vanke A and Kweichou Moutai. Adopting mean square error and average absolute percentage error as criteria, we find BP neural network consistently and robustly outperforms the other four models.