Add to Chrome

Add to Chrome Add to Firefox

Add to Firefox Add to Edge

Add to EdgeRuihao Zhu

Efficient and Interpretable Bandit Algorithms

Oct 23, 2023

Motivated by the importance of explainability in modern machine learning, we design bandit algorithms that are \emph{efficient} and \emph{interpretable}. A bandit algorithm is interpretable if it explores with the objective of reducing uncertainty in the unknown model parameter. To quantify the interpretability, we introduce a novel metric of \textit{uncertainty loss}, which compares the rate of the uncertainty reduction to the theoretical optimum. We propose CODE, a bandit algorithm based on a \textbf{C}onstrained \textbf{O}ptimal \textbf{DE}sign, that is interpretable and maximally reduces the uncertainty. The key idea in \code is to explore among all plausible actions, determined by a statistical constraint, to achieve interpretability. We implement CODE efficiently in both multi-armed and linear bandits and derive near-optimal regret bounds by leveraging the optimality criteria of the approximate optimal design. CODE can be also viewed as removing phases in conventional phased elimination, which makes it more practical and general. We demonstrate the advantage of \code by numerical experiments on both synthetic and real-world problems. CODE outperforms other state-of-the-art interpretable designs while matching the performance of popular but uninterpretable designs, such as upper confidence bound algorithms.

User Experience Design Professionals' Perceptions of Generative Artificial Intelligence

Sep 26, 2023Among creative professionals, Generative Artificial Intelligence (GenAI) has sparked excitement over its capabilities and fear over unanticipated consequences. How does GenAI impact User Experience Design (UXD) practice, and are fears warranted? We interviewed 20 UX Designers, with diverse experience and across companies (startups to large enterprises). We probed them to characterize their practices, and sample their attitudes, concerns, and expectations. We found that experienced designers are confident in their originality, creativity, and empathic skills, and find GenAI's role as assistive. They emphasized the unique human factors of "enjoyment" and "agency", where humans remain the arbiters of "AI alignment". However, skill degradation, job replacement, and creativity exhaustion can adversely impact junior designers. We discuss implications for human-GenAI collaboration, specifically copyright and ownership, human creativity and agency, and AI literacy and access. Through the lens of responsible and participatory AI, we contribute a deeper understanding of GenAI fears and opportunities for UXD.

Phase Transitions in Learning and Earning under Price Protection Guarantee

Nov 03, 2022

Motivated by the prevalence of ``price protection guarantee", which allows a customer who purchased a product in the past to receive a refund from the seller during the so-called price protection period (typically defined as a certain time window after the purchase date) in case the seller decides to lower the price, we study the impact of such policy on the design of online learning algorithm for data-driven dynamic pricing with initially unknown customer demand. We consider a setting where a firm sells a product over a horizon of $T$ time steps. For this setting, we characterize how the value of $M$, the length of price protection period, can affect the optimal regret of the learning process. We show that the optimal regret is $\tilde{\Theta}(\sqrt{T}+\min\{M,\,T^{2/3}\})$ by first establishing a fundamental impossible regime with novel regret lower bound instances. Then, we propose LEAP, a phased exploration type algorithm for \underline{L}earning and \underline{EA}rning under \underline{P}rice Protection to match this lower bound up to logarithmic factors or even doubly logarithmic factors (when there are only two prices available to the seller). Our results reveal the surprising phase transitions of the optimal regret with respect to $M$. Specifically, when $M$ is not too large, the optimal regret has no major difference when compared to that of the classic setting with no price protection guarantee. We also show that there exists an upper limit on how much the optimal regret can deteriorate when $M$ grows large. Finally, we conduct extensive numerical experiments to show the benefit of LEAP over other heuristic methods for this problem.

Learning to Price Supply Chain Contracts against a Learning Retailer

Nov 02, 2022

The rise of big data analytics has automated the decision-making of companies and increased supply chain agility. In this paper, we study the supply chain contract design problem faced by a data-driven supplier who needs to respond to the inventory decisions of the downstream retailer. Both the supplier and the retailer are uncertain about the market demand and need to learn about it sequentially. The goal for the supplier is to develop data-driven pricing policies with sublinear regret bounds under a wide range of possible retailer inventory policies for a fixed time horizon. To capture the dynamics induced by the retailer's learning policy, we first make a connection to non-stationary online learning by following the notion of variation budget. The variation budget quantifies the impact of the retailer's learning strategy on the supplier's decision-making. We then propose dynamic pricing policies for the supplier for both discrete and continuous demand. We also note that our proposed pricing policy only requires access to the support of the demand distribution, but critically, does not require the supplier to have any prior knowledge about the retailer's learning policy or the demand realizations. We examine several well-known data-driven policies for the retailer, including sample average approximation, distributionally robust optimization, and parametric approaches, and show that our pricing policies lead to sublinear regret bounds in all these cases. At the managerial level, we answer affirmatively that there is a pricing policy with a sublinear regret bound under a wide range of retailer's learning policies, even though she faces a learning retailer and an unknown demand distribution. Our work also provides a novel perspective in data-driven operations management where the principal has to learn to react to the learning policies employed by other agents in the system.

Risk-Aware Linear Bandits: Theory and Applications in Smart Order Routing

Aug 04, 2022

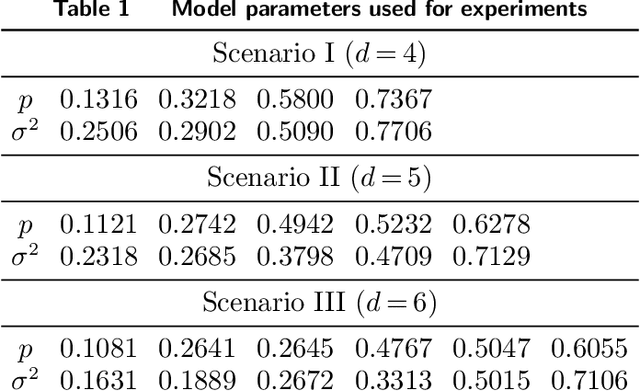

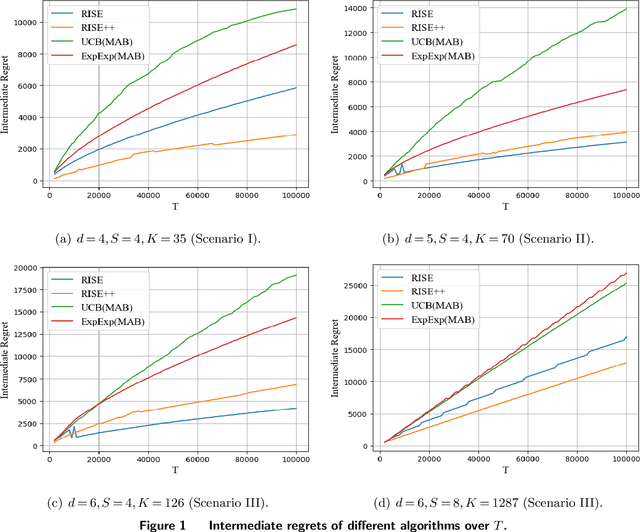

Motivated by practical considerations in machine learning for financial decision-making, such as risk-aversion and large action space, we initiate the study of risk-aware linear bandits. Specifically, we consider regret minimization under the mean-variance measure when facing a set of actions whose rewards can be expressed as linear functions of (initially) unknown parameters. Driven by the variance-minimizing G-optimal design, we propose the Risk-Aware Explore-then-Commit (RISE) algorithm and the Risk-Aware Successive Elimination (RISE++) algorithm. Then, we rigorously analyze their regret upper bounds to show that, by leveraging the linear structure, the algorithms can dramatically reduce the regret when compared to existing methods. Finally, we demonstrate the performance of the algorithms by conducting extensive numerical experiments in a synthetic smart order routing setup. Our results show that both RISE and RISE++ can outperform the competing methods, especially in complex decision-making scenarios.

Safe Optimal Design with Applications in Policy Learning

Nov 08, 2021

Motivated by practical needs in online experimentation and off-policy learning, we study the problem of safe optimal design, where we develop a data logging policy that efficiently explores while achieving competitive rewards with a baseline production policy. We first show, perhaps surprisingly, that a common practice of mixing the production policy with uniform exploration, despite being safe, is sub-optimal in maximizing information gain. Then we propose a safe optimal logging policy for the case when no side information about the actions' expected rewards is available. We improve upon this design by considering side information and also extend both approaches to a large number of actions with a linear reward model. We analyze how our data logging policies impact errors in off-policy learning. Finally, we empirically validate the benefit of our designs by conducting extensive experiments.

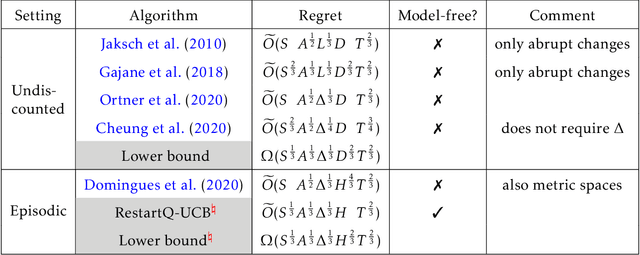

Near-Optimal Regret Bounds for Model-Free RL in Non-Stationary Episodic MDPs

Oct 07, 2020

We consider model-free reinforcement learning (RL) in non-stationary Markov decision processes (MDPs). Both the reward functions and the state transition distributions are allowed to vary over time, either gradually or abruptly, as long as their cumulative variation magnitude does not exceed certain budgets. We propose an algorithm, named Restarted Q-Learning with Upper Confidence Bounds (RestartQ-UCB), for this setting, which adopts a simple restarting strategy and an extra optimism term. Our algorithm outperforms the state-of-the-art (model-based) solution in terms of dynamic regret. Specifically, RestartQ-UCB with Freedman-type bonus terms achieves a dynamic regret of $\widetilde{O}(S^{\frac{1}{3}} A^{\frac{1}{3}} \Delta^{\frac{1}{3}} H T^{\frac{2}{3}})$, where $S$ and $A$ are the numbers of states and actions, respectively, $\Delta>0$ is the variation budget, $H$ is the number of steps per episode, and $T$ is the total number of steps. We further show that our algorithm is near-optimal by establishing an information-theoretical lower bound of $\Omega(S^{\frac{1}{3}} A^{\frac{1}{3}} \Delta^{\frac{1}{3}} H^{\frac{2}{3}} T^{\frac{2}{3}})$, which to the best of our knowledge is the first impossibility result in non-stationary RL in general.

Reinforcement Learning for Non-Stationary Markov Decision Processes: The Blessing of (More) Optimism

Jun 24, 2020

We consider un-discounted reinforcement learning (RL) in Markov decision processes (MDPs) under drifting non-stationarity, i.e., both the reward and state transition distributions are allowed to evolve over time, as long as their respective total variations, quantified by suitable metrics, do not exceed certain variation budgets. We first develop the Sliding Window Upper-Confidence bound for Reinforcement Learning with Confidence Widening (SWUCRL2-CW) algorithm, and establish its dynamic regret bound when the variation budgets are known. In addition, we propose the Bandit-over-Reinforcement Learning (BORL) algorithm to adaptively tune the SWUCRL2-CW algorithm to achieve the same dynamic regret bound, but in a parameter-free manner, i.e., without knowing the variation budgets. Notably, learning non-stationary MDPs via the conventional optimistic exploration technique presents a unique challenge absent in existing (non-stationary) bandit learning settings. We overcome the challenge by a novel confidence widening technique that incorporates additional optimism.

Reinforcement Learning under Drift

Jun 07, 2019

We propose algorithms with state-of-the-art \emph{dynamic regret} bounds for un-discounted reinforcement learning under drifting non-stationarity, where both the reward functions and state transition distributions are allowed to evolve over time. Our main contributions are: 1) A tuned Sliding Window Upper-Confidence bound for Reinforcement Learning with Confidence-Widening (\texttt{SWUCRL2-CW}) algorithm, which attains low dynamic regret bounds against the optimal non-stationary policy in various cases. 2) The Bandit-over-Reinforcement Learning (\texttt{BORL}) framework that further permits us to enjoy these dynamic regret bounds in a parameter-free manner.

Hedging the Drift: Learning to Optimize under Non-Stationarity

Mar 04, 2019

We introduce general data-driven decision-making algorithms that achieve state-of-the-art \emph{dynamic regret} bounds for non-stationary bandit settings. It captures applications such as advertisement allocation and dynamic pricing in changing environments. We show how the difficulty posed by the (unknown \emph{a priori} and possibly adversarial) non-stationarity can be overcome by an unconventional marriage between stochastic and adversarial bandit learning algorithms. Our main contribution is a general algorithmic recipe that first converts the rate-optimal Upper-Confidence-Bound (UCB) algorithm for stationary bandit settings into a tuned Sliding Window-UCB algorithm with optimal dynamic regret for the corresponding non-stationary counterpart. Boosted by the novel bandit-over-bandit framework with automatic adaptation to the unknown changing environment, it even permits us to enjoy, in a (surprisingly) parameter-free manner, this optimal dynamic regret if the amount of non-stationarity is moderate to large or an improved (compared to existing literature) dynamic regret otherwise. In addition to the classical exploration-exploitation trade-off, our algorithms leverage the power of the "forgetting principle" in their online learning processes, which is vital in changing environments. We further conduct extensive numerical experiments on both synthetic data and the CPRM-12-001: On-Line Auto Lending dataset provided by the Center for Pricing and Revenue Management at Columbia University to show that our proposed algorithms achieve superior dynamic regret performances.